Budgeting and frugal living can help you pay off debt, even without a high income.

An abbreviated version of this post was originally posted on Medium. This post may contain affiliate links. Please see our disclosures for more information.

I was in panic mode back in August of 2015.

At the time, my 11-month Fulbright grant overseas in Taiwan was ending, which meant my student loan deferment period was also drawing to a close. After graduating from college the previous year, the Fulbright scholarship had granted me temporary relief from that looming debt. (Since the scholarship was considered a graduate scholarship, I’d been able to apply for loan deferment.)

Unfortunately, while serving out the grant, I had been a dummy and left my loans untouched during that holy deferment period, unaware that interest had been steadily accruing.

That meant returning to an ugly reality once I returned to the U.S.: a $15,380.72 debt.

Thankfully, I had scored a job offer with an education nonprofit and was due to start just a few weeks after returning home to Houston. And though a daunting endeavor, I was committed to paying off that debt asap.

I succeeded in a year — well, technically, just over a year, with my first payment on July 22, 2015, and my last on July 27, 2016. Though my balance started at about $15,381, I ultimately ended up paying $16,218.53 because of interest.

Before I dive into the details of paying off my loans, a quick note:

I’m not a financial professional by any means . I n fact, most of my financial knowledge has come from the internet (specifically, Reddit’s personal finance and financial independence subreddits). I therefore am not prescribing that student debt-holders follow the same course of repayment. This is simply a personal account of how I handled my own repayment quest.

Here’s how I did it on a nonprofit salary.

I tracked my finances.

Tracking finances alone did not speed up paying off my student loans. However, what it did do was make me incredibly cognizant of where my money was going and what I could afford to cut back on.

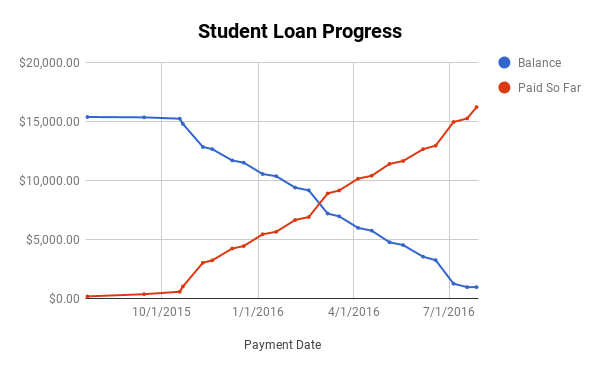

I kept an eye on my expenses using the app Monefy and exported every month’s financial breakdown into a master spreadsheet on my laptop, complete with a line graph of my loan repayment progress. Here’s what that graph looked like:

Nothing fancy or complicated—just a progress chart created using Google Sheets.

Though I never set hard limits on my spending categories, I compared them across different months and kept a mental list of what to watch out for. So if I noticed I spent more eating out in February, for instance, I’d make it a point to cook more in March.

The level of meticulousness involved with recording my paychecks and expenses probably sounds intense — but sometimes I found a weird sense of enjoyment in reviewing the data. It was incredibly satisfying to see “leftover” money from each month and know that I could contribute more to my loans as well as savings.

I lived with a roommate.

I rented the master bedroom in a two-room apartment that cost $995 total (excluding utilities), though living with a roommate reduced that housing expense considerably. Since the other room was smaller and likely intended as a study, not a second bedroom, my rent was higher — $570 — yet this was by all means still a steal considering that rent in Houston averages over $1,000.

My apartment was in a gated community and included a pool, but its location was the best part. Not only was my company’s office nearby, but so was the grocery store, gym, and even the Houston Galleria, Texas’s largest shopping mall (although I didn’t frequent it often). The sheer convenience of living so close to these places further reduced transportation costs because I simply didn’t have to drive far to get to the mainstays of my day-to-day life.

I didn’t get a car.

Houston is known for its urban sprawl and lacking public transit. Owning and driving a car there is the norm, so to my family and friends, it was certainly a bold move to forgo one.

Instead, I bought a 150cc motor scooter.

Having spent the previous year in scooter-rampant Taiwan, I’d gotten a Taiwanese scooter license — and it just so happened that Texas and Taiwan share licensing reciprocity. As a result, I smoothly transferred my Taiwanese scooter license over into an American motorcycle license.

In spite of how unconventional it was, I opted to drive a scooter in Houston. Given the cost of car ownership and maintenance, choosing this alternative means of transportation was significantly cheaper and on top of that, more eco-friendly. The scooter itself was $1,020, although full disclosure: my mom bought it for me and refused my attempts to repay her later on, a privilege that I am endlessly grateful for.

Besides choosing not to buy a car, I managed to find an apartment just under a mile away from my workplace, which lowered my gas expenses. As a result, with the occasional Uber ride and scooter repair, transportation expenses typically averaged less than $80 per month.

I cooked instead of eating out.

Just about every guide to frugality and personal finance advises eating out less in order to save. And for good reason, too — my groceries averaged just under $200 per month, or roughly $50 per week. On the other hand, eating out cost me anywhere from $8 to $25 depending on the type of restaurant.

I didn’t give up on dining out altogether, though. In fact, I still ate out with friends, but avoided doing so in excess. Except for an occasional splurge month, that generally meant eating out just once or twice a week.

Since eating is in many cases a social activity, did that mean my social life took a hit?

Not at all. Instead of going out, I’d invite friends over for a home-cooked meal, or suggest dessert outings in place of dinner dates (all the better for my sweet tooth). For a while, I even did mystery shopping at certain bars and restaurants. This meant I could still eat out with friends but get reimbursed (and rack up credit card points at the same time).

I picked up more than one side hustle.

If I had paid the same amount towards my student loans every month ($16,218.53 ÷ 12), that would have equated to a monthly student loan payment of about $1,351.

That would also have been about half of my monthly nonprofit salary at the time.

If that sounds unreasonable, that’s because it is — you’d need a fortuitous combination of circumstances (e.g., living at home and not paying for rent or bills) to be able to devote 50% of your monthly income just to student loans.

So I didn’t do that. Instead, I increased my monthly income by taking up part-time jobs over the course of the year:

- Copy editing – I landed my first copy editing gig through a combination of luck and initiative. I reached out to an online publication that had pieces rife with typos, and expressed interest in helping to edit their work. Though I was initially rejected, I eventually got hired as a freelance copy editor. Several months later, a former coworker posted a Facebook status advertising her search for freelance editors. I responded and after taking a test, scored another client.

- Teaching – I took a part-time role at a language school in the spring of 2016, teaching a few classes in English and art to young children and adults. Classes took place on Saturday mornings and afternoons—a sacrifice I was willing to make to pay off my loans faster. It wasn’t terrible, though; since the job ran according to an academic calendar, my summer weekends were free.

My income increased anywhere from an additional $100 to over $700 per month as a result of taking up these side hustles. That meant I could chip in a second monthly payment towards my student loans — but also not starve.

I looked for ways to lower my bills.

Specifically, I:

- Opted for a super cheap phone plan. I paid $32 a month for a plan with Ultra Mobile. It didn’t have unlimited data, but I was fine with that.

- Adjusted my thermostat based on the season. That meant living through a hot summer and a cold winter in order to reduce my electricity bill. There were still a few expensive months (summer in Houston, go figure), but on the whole, I avoided blasting the A/C or heating. It also helped to split this cost (as well as Wi-Fi) with a roommate.

- Joined an inexpensive gym. The closest gym, the YMCA, was conveniently half a mile from my apartment and cost me $35 a month. Moreover, I got lucky and happened to join on a weekend when the $75 signup fee was waived. Of course, there are cheaper gym options out there, but this still beat the average monthly boutique fitness membership and $50+ spent on gyms.

- Didn’t pay for cable or any streaming services like Hulu or Netflix. I didn’t own a television (or even watch much to begin with) — but if the mood struck, I occasionally caught full episodes of whatever was available on NBC or some other network’s website.

I arranged my social life according to my finances.

Though having more money for discretionary spending certainly allows for a greater variety of social activities, repaying my loans didn’t mean sacrificing my social life altogether. In fact, I regularly saw my friends and even traveled during my repayment year, making trips to D.C., Zion National Park, Austin, and even Taiwan.

Provided that I didn’t go crazy with spending, going on trips was still very much possible. Aside from that, arranging my social life based on finances just meant:

- Having friends over for dinner instead of going out to eat

- Limiting nights at the movies

- Ordering fewer drinks when out on the town

- Borrowing books from the local public library instead of buying them

Lastly, I lived frugally.

In other words, I practiced some frugal day-to-day habits that led to larger savings in the long run. That included:

- Rarely buying clothing. In general, I wanted to reduce my wardrobe and thus, rarely bought clothes. If I bought clothes, I almost always bought items on sale or from Goodwill.

- Using credit cards with decent cash-back deals. I generally avoided cards without annual fees (except for one airline credit card). Moreover, I almost always paid with card to reap the benefits of their cash-back deals.

- Paying all credit card balances in full. Speaking of credit cards, I always paid off my balances in full rather than letting any debt accumulate.

- Staying with friends or splitting accommodation costs while traveling.

- Drinking mostly water. I just about always drank water — no daily cup of coffee to start the day or glass of red wine to end it.

- Cutting my own hair.

On their own, perhaps these habits don’t seem to mean much. But in the long run, they stack up and can save hundreds, even thousands, of dollars that would be better spent paying off debt.

I had less debt than my average peer ($28,950 for 2014 graduates), but that didn’t stop that $16,000-loan from haunting me. While paying it off meant sacrificing some short-term luxuries (for instance, my Saturday mornings spent on my teaching side hustle), it ultimately meant peace of mind in the long run… A luxury that’s been well worth it.

Really Inspirational story for all 45 million student debtors, including myself!

Congrats on paying off all of that student loan debt so quickly!

Thanks so much, Nate!