There’s a retirement savings gap between men and women—but narrowing and closing it could benefit everyone.

In 2022, March 15 marked Equal Pay Day—the symbolic day of how far into the year women must work in order to earn what men earned the previous year.

Unfortunately, it’s not quite as straightforward as it seems. That’s because this single day doesn’t account for differences in pay based on race, which further affects how far into the year women must work to achieve equal pay. In fact:

- For black women, Equal Pay Day falls on September 21.

- Native Women’s Equal Pay Day is December 1.

- Finally, Latinas’ Equal Pay Day is December 8.

The existence of Equal Pay Day itself underscores the reality of the wage gap, which more than a quarter of Americans shockingly believe is a myth.

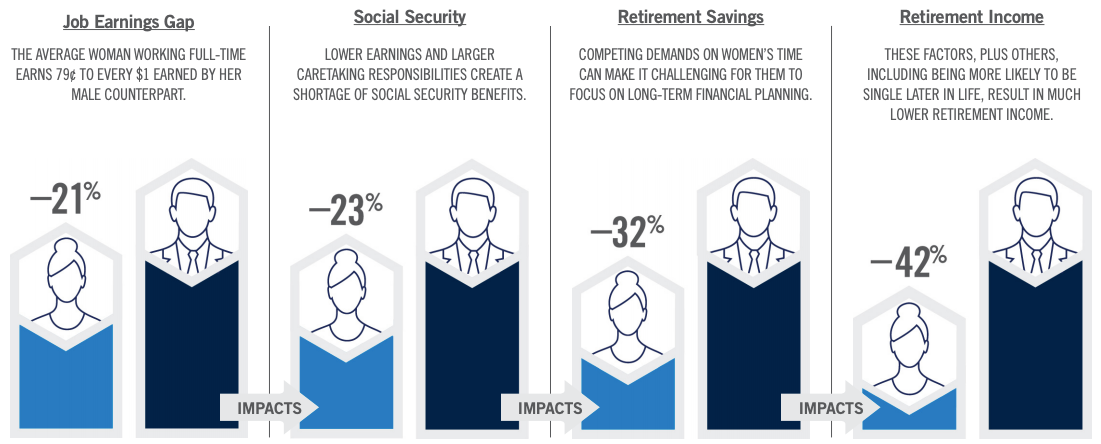

But the very real wage gap has unfortunate concrete ramifications—for starters, the disparity in retirement savings between women and men.

The Retirement Savings Gap

If you’re skeptical of the retirement savings gap between men and women, there’s plenty of data supporting its existence.

Take a look:

- A study by Merrill Lynch estimates an approximate $1,055,000 gap in cumulative lifetime earnings between men and women. Such a gap explains in part why a difference in retirement savings exists: by virtue of earning less, women have less to save for retirement.

- According to Prudential, the retirement account balance of female employees is on average, one-third less than that of male employees’.

- In the U.S., the average woman earns less from Social Security benefits than the average man. While more than half of women receive less than $1,000 in Social Security benefits, the average man earns $1,500.

(Image credit: Fool / Social Security Administration)

Why does a retirement gender gap exist?

The savings gap can be attributed to a confluence of mostly social factors, namely the following four.

- Women earn less than men. Though the gender wage gap has narrowed since 1980, women continue to make about 85% of what men earn. According to the Pew Research Center, the wage gap can be in part attributed to differences in educational attainment, occupational segregation, and work experience. However, gains by women in these areas have helped to narrow the gap somewhat, although ongoing factors like gender discrimination contribute to its persistence.

- Women have longer life expectancies. On average, women tend to outlive men by nearly seven years. Why? Thanks to hormones and genetic makeup, women appear to have a natural biological advantage, although it’s unclear exactly how much. But biology aside, demographers point to culture and socialization to explain gender differences in longevity. For instance, society encourages men to participate in certain behaviors more than women, some of which can be dangerous or harmful.

- Women tend to take off more time from work for parenthood and caregiving. This is due to traditional gender roles and the fact that the U.S. is notoriously the only developed country in the world that does not mandate paid maternity leave. Moreover, paternity leave policies remain lacking, and in doing so, reinforce the notion that women should leave the workforce to take care of their kids. Some states have independently enacted maternity and family leave policies, but the extent of their coverage and benefits varies. Lastly, outside of parenthood, caregiving, whether for an elderly or ill relative, is also female-dominated. According to a 2015 report by the AARP, 60% of caregivers are women.

- Women are increasingly sole or primary breadwinners. According to the Center for American progress, 42% of women brought in at least half of their family’s earnings in 2015. At face value, this might suggest we’re getting closer to achieving gender parity in the workforce—but that’s not correct. Since 1974, the amount of married couples heading households has decreased from 84% to 65.5% in 2015; meanwhile, the number of single-mom families grew from 14.6% to 26.4% in the same time frame. This shift in family dynamics means more working mothers, who, besides facing a wage gap and higher life expectancy on average, must also bear the majority of child-related and caregiving costs. As a result, breadwinning mothers generally have less savings to set aside for retirement.

It’s fair to say some, if not all, of these factors are changing—but they’re still very much a work in progress.

(Image credit: Prudential)

What about gender differences in investing?

Some research suggests there are gender differences in the ways men and women invest, albeit with conflicting results. At a professional level, it appears that male- and female-managed funds face comparable outcomes, although the decision-making behaviors between them varies. Individually, the findings are hazier.

For one, there’s the longstanding conception of women being more risk-averse and conservative than men.

But more and more social scientists are challenging this idea.

For instance, research by Betterment suggests that women are less prone to changing their asset allocation in automated portfolios. This theoretically makes them more successful at long-term investing. Similarly, a study by Fidelity found that women marginally outperformed men by 0.4% in their investments.

Yet in spite of these findings, women continue to report feeling less confident about their investing choices than men. Whereas 68% of men feel confident about managing their assets, only 52% of women feel similarly.

(Image credit: Merrill Lynch)

Confidence certainly does not translate into competence, of course, but a shortage on confidence can translate into negative outcomes. Consider, for example, someone who’s competent in investing but lacks confidence; they might be more easily persuaded into buying financial services they don’t need.

Why do people need to know about this savings gap?

The obvious reason: knowing about this gap is important for retirement planning.

There are a number of online retirement calculators that help estimate how much is needed for one to safely retire—AARP, Vanguard, and Bankrate, to name a few. But as helpful as these tools are, they generally aren’t nuanced enough to account for the gender gap in retirement savings.

That means people who base their retirement goals on the results of these calculators may be underestimating the total amount needed for a secure retirement.

But knowing about the savings gap isn’t important only for the sake of retirement planning.

Like the champagne glass distribution of wealth, the retirement savings gap is another example of wealth inequality. Being aware of it is important for framing larger social and political discussions as well as shaping personal finance education in the future.

In spite of the abundance of research and data, there are skeptics, made up of both men and women, of the gender wage gap and its larger implications. However, the more people who are aware of these disparities, the more steps can be taken toward creating policies and initiatives that benefit both genders, e.g., family leave policies.

I’d never thought that hard about this gap before. My mother is taking a surprise early retirement package soon. I can really see her in a lot of this information. Thanks for spreading this information.

In spite of hearing about the gender wage gap before, I’d never thought too much about the retirement gap either. And I’m glad this article could help—thanks for reading!

The difference in investing styles is very interesting! Long term, women would definitely come out ahead by holding. Very informative, thank you!

Glad you got something out of this—thanks for reading!

Hi Financial Impulse, great post. In regards retirement calculators, one certainly needs to be careful with the results of them. These calculators are normally just the compound interest formula and therefore require a constant rate of return as an input. But there isn’t a growth investment around that can provide that. So basing your retirement aspirations on their results could be disappointing over the long term.

Thanks for stopping by, Adrian! You’re absolutely right—we definitely need to be cautious when using retirement calculators.